Frank Tam | December 2025

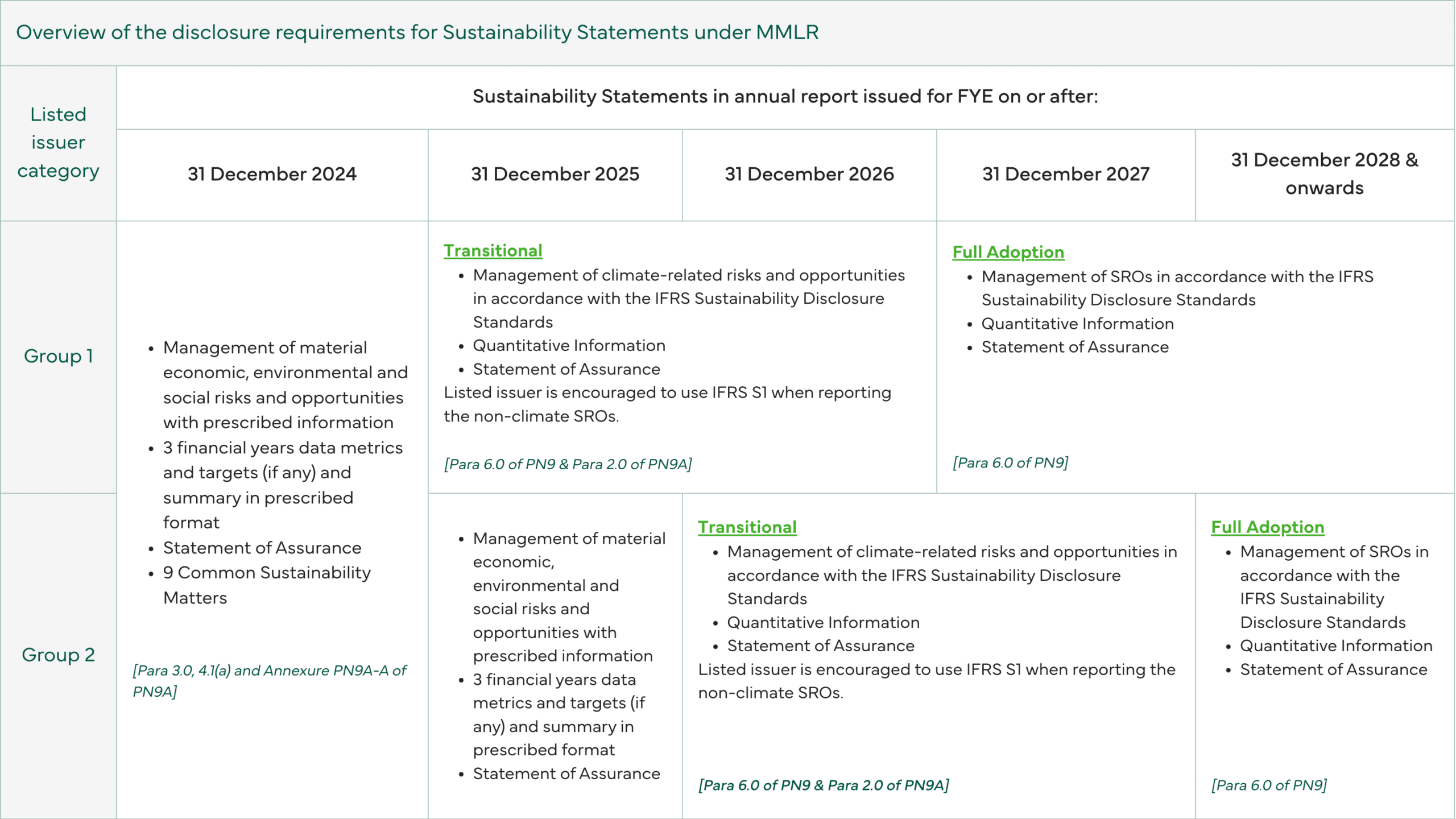

The implementation timeline is tiered based on market capitalisation and market board.

Determine which category your company falls into:

Adoption is not immediate for everyone. The framework utilises a phased approach, meaning smaller companies have a longer runway to prepare data and systems.

| Category | First Financial Year Ending (FYE) for implementation of NSRF |

|---|---|

|

Group 1 |

FYE ending on or after 31 December 2025 |

|

Group 2 |

FYE ending on or after 31 December 2026 |

|

ACE Market |

ACE Market FYE ending on or after 31 December 2027 |

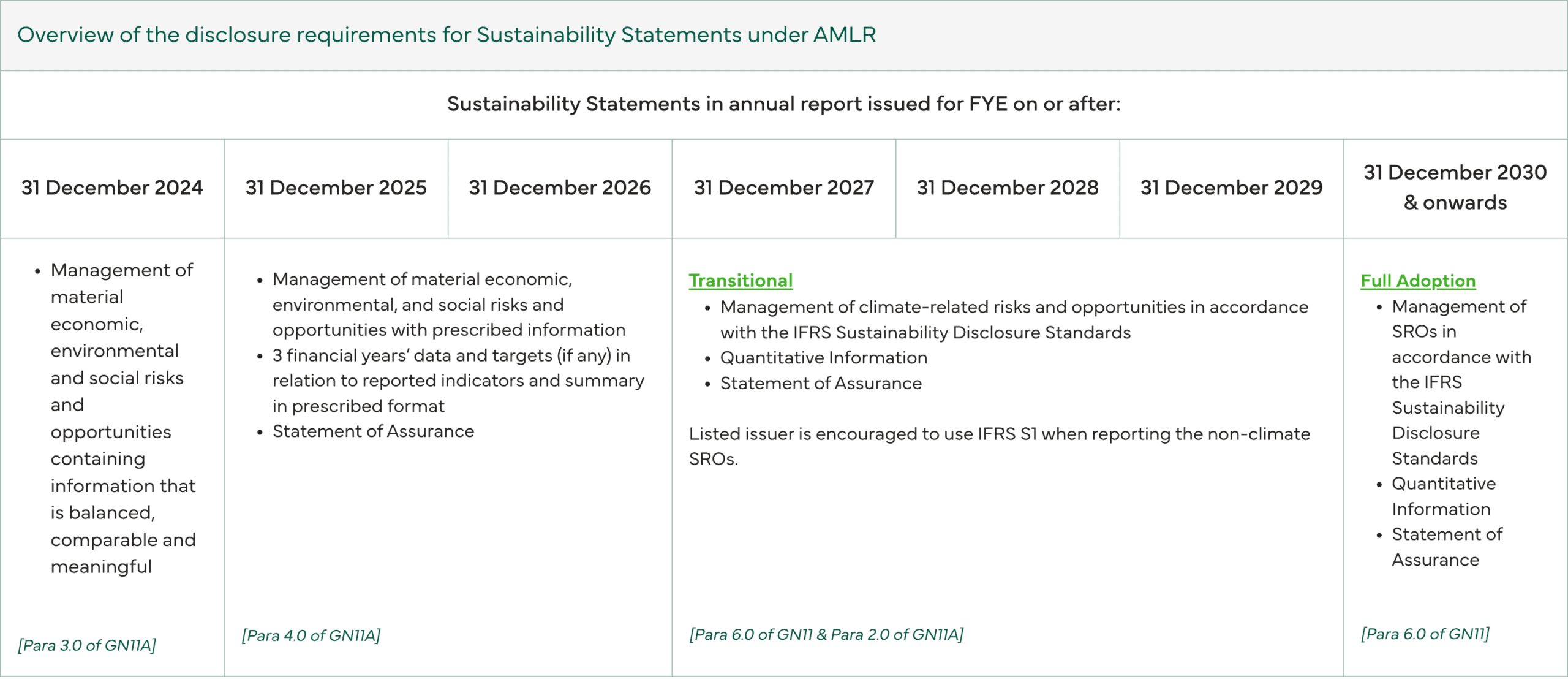

Note on Pre-Transition Reporting: Until your specific effective date arrives, you must continue reporting under the existing Bursa Malaysia sustainability framework.

Main Market (Group 2): Continue disclosing the “Common Sustainability Matters” and 3 years of data through FYE 2025.

ACE Market: Maintain current disclosures through FYE 2026. Notably, the requirement to provide TCFD-aligned disclosures (originally planned for 2027) has been disapplied to allow you to focus directly on preparing for IFRS S2.

Recognising that full IFRS compliance is a heavy lift, the NSRF allows all issuers to adopt a “Climate-First” approach during their initial years of adoption.

Regardless of whether you are Group 1, 2, or ACE, when you hit your effective date, you can utilise the following Additional Transition Reliefs (ATRs):

A common question is “If we use the relief to report only on climate (IFRS S2), do we ignore other sustainability issues?”

No. While you transition to IFRS S2 for climate, you must continue to report on other material sustainability matters (e.g., labor practices, anti-corruption, diversity).

However, for FYE 2025, these non-climate matters will continue to be reported under the existing Bursa Malaysia “Common Sustainability Matters” framework, not yet under the full IFRS S1 methodology.

Trust in data is as important as the data itself. The NSRF sets out a roadmap for mandatory reasonable assurance on Scope 1 and Scope 2 GHG emissions. This will move sustainability reporting closer to the rigour of financial auditing.

| Category | Category Mandatory Reasonable Assurance Begins |

|---|---|

|

Group 1 |

FYE ending on or after 31 December 2027 |

|

Group 2 |

Group 2 FYE ending on or after 31 December 2028 |

|

ACE Market |

ACE Market FYE ending on or after 31 December 2029 |

(Note: These dates are subject to final confirmation following further consultation by the ACSR through a dedicated sub-committee led by AOB.)

Even if you are in Group 2 or the ACE Market with years to spare, the complexity of IFRS S2 requires early action.

You should use 2025 to perform a “dry run.” Assess your data gaps against IFRS S2 requirements. Since TCFD-aligned disclosures are disapplied, pivot your resources immediately toward IFRS S2 gap analysis.

While you have the longest runway, you often have fewer resources. Use the PACE (Policy, Assumptions, Calculators, Education) resources provided by the Securities Commission to upskill your team without incurring high consultancy costs.

Does your Board understand these timelines? The new framework requires a cross-functional approach involving finance, risk, and sustainability teams.

The FYE 2025 deadline represents a significant step up in compliance for Malaysia’s large listed issuers (Group 1). By leveraging the available transition reliefs specifically the “climate-first” approach, Group 1 companies can manage this transition effectively focusing resources on building robust climate data foundations before expanding to full IFRS S1 adoption in 2027.

To help visualise the timeline, the following tables summarise the transition from the existing framework to full IFRS S1 & S2 adoption for different groups.

Implementation is split into two (2) groups based on market capitalisation.

ACE Market issuers have a longer runway maintaining the current “Common Sustainability Matters” framework through FYE 2026.